Cracker Barrel’s three-year transformation plan, budgeted at $600–$700 million in capital spending, was always going to be a moonshot. Set against a market capitalization that hovered around $1.2–$1.3 billion in late August 2025, the company effectively wagered roughly half of its equity value on a turnaround executed in full public view. That scale alone made the program a very risky endeavor even before the brand-identity backlash of the past week.

Cracker Barrel CEO Julie Felss Masino being interviewed – YouTube, TODAY

READ: Former Superman Actor Tyler Hoechlin Wants to Play Batman in James Gunn’s DCU

Announced on May 16, 2024, the plan aimed to “refine the brand,” overhaul menus, remodel stores, upgrade tech, and improve the employee experience—ambitions large enough to demand a reset of capital priorities. To fund the work, the board slashed the quarterly dividend from $1.30 to $0.25 (an ~80% cut), signaling that cash once returned to shareholders would be plowed back into the business for several years. Management’s guidance put total capex at $600–$700 million from FY2025–FY2027, with benefits not really accelerating until late FY2026 into FY2027. That cadence increases execution risk: investors are asked to be patient while the P&L absorbs years of elevated depreciation and remodel disruption.

Cracker Barrel’s 93-year-old founder has some strong words for the CEO trying to rebrand and modernize… pic.twitter.com/hHoGl8b4B5

— End Wokeness (@EndWokeness) August 28, 2025

The underlying operating base wasn’t robust, either. In FY2024, comparable restaurant sales were down 0.1% despite nearly 5% pricing, and comparable retail sales fell 5.5%… a sign that traffic softness and shop weakness were real headwinds. Cracker Barrel also closed some stores and took related charges as it reviewed the portfolio. With roughly 660 locations across the U.S., even modest misfires in remodel design or menu positioning can echo through the system.

The new logo for Cracker Barrel – YouTube, TODAY

READ: Power Surge Causes Chaos at Walt Disney World: 40+ Attractions Down, Monorails Suspended

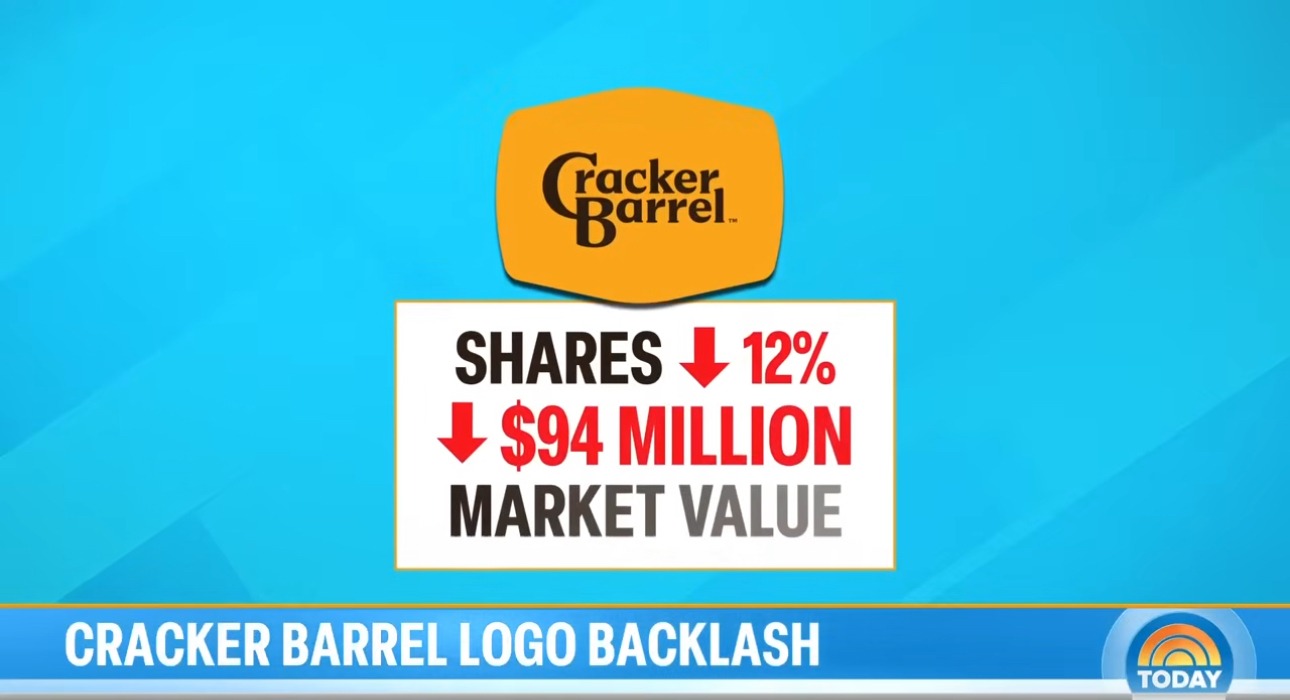

Then came the branding stumble. In August 2025, Cracker Barrel unveiled a minimalist logo intended to modernize the chain and appeal to younger diners. The immediate reaction was severe: shares fell sharply, wiping out close to $100 million in market value, and critics framed the move as abandoning the company’s heritage. Within days, the company reverted to its legacy logo, effectively U-turning on a centerpiece of the “refine the brand” pillar. Regardless of one’s view of the politics around it, the episode underscores how fragile brand equity can be, and how costly a misread becomes when it’s attached to a $700M transformation.

Now fire your CEO and we’ll all come back. pic.twitter.com/W3AveWvmDM

— Jeremy Prime (@DDayCobra) August 26, 2025

From a capital-allocation perspective, this is why the wager looked so perilous. When a small-cap company earmarks a sum approaching 50–60% of its market cap to overhaul brand, menu, and four-wall experiences, the plan must land almost flawlessly. The dividend reset reduced financial flexibility for shareholders, while the public reversal on the logo suggests stakeholder alignment—customers, employees, investors—was not fully secured before launch. Those process failures increase the probability that the return on invested capital falls short of the hurdle rate, turning a bold bet into value destruction. Outside critics were already warning the board in 2024–2025 that the strategy risked being more sizzle than steak.

The stock drop after Cracker Barrel rebranded its iconic logo – YouTube, TODAY

READ: The Semi-Hidden Truth Behind Six Flags’ Park Closings: Follow The Money

To be fair, not all signals are negative (yet). Management has reported pockets of stabilization: in Q3 FY2025, comparable restaurant sales turned +1.0% year-over-year (though retail comps remained –3.8%). If remodels ultimately drive throughput and the menu gets traction once the turmoil passes (now unlikely given the scale), the earnings algorithm could improve into FY2027 as guided. But the early-stage financials look mixed, and the brand whiplash complicates the path to consistent traffic growth.

The iconic rocking chairs outside Cracker Barrel – YouTube, TODAY

Viewed in total, Cracker Barrel bet an extraordinary sum for a company of its size, on a timeline that required near-perfect execution and change-management discipline. The rapid logo reversal—after a very public sell-off—suggests the company underestimated the risk of alienating its core while courting a new audience. With capex commitments still large and the dividend reset fresh, the margin for error remains thin. For a ~$1.2–$1.3B chain, staking $700M on a brand and box-level reinvention was always going to be risky; events this month show just how quickly that risk can crystallize.

One might say Cracker Barrel bet the farm… and lost everything but the beans.

UP NEXT: Miles Morales Adidas Suit in Spider-Man 2 Draws Backlash from Fans — and Even His Voice Actor

{kind=link}