A newly released Paramount SEC filing regarding its hostile takeover tender offer for WBD has ignited a firestorm around Warner Bros. Discovery’s handling of its proposed sale to Netflix. According to the document, Paramount submitted an improved $30-per-share all-cash offer on December 4th—an offer specifically crafted to address every concern WBD had previously raised. But the filing alleges something extraordinary: WBD’s board never responded. Not a counter. Not a question. Not even a courtesy acknowledgment.

Instead, by the very next morning, WBD announced it had reached an agreement with Netflix.

A graphic showing the Netflix and Warner Bros. Logos – Netflix

READ: Jimmy Kimmel Renewed by ABC — But It’s Not the Triumph the Media is Framing It As

For shareholders, this sequence isn’t just eyebrow-raising. It cuts straight to the heart of corporate governance. When a board receives a financially superior offer—one with higher cash value, stronger certainty, and fully committed financing—and chooses not to engage, what does that say about the integrity of the sale process?

According to the Paramount SEC filing, it suggests something deeply concerning for WBD shareholders.

A Timeline That Raises Serious Questions

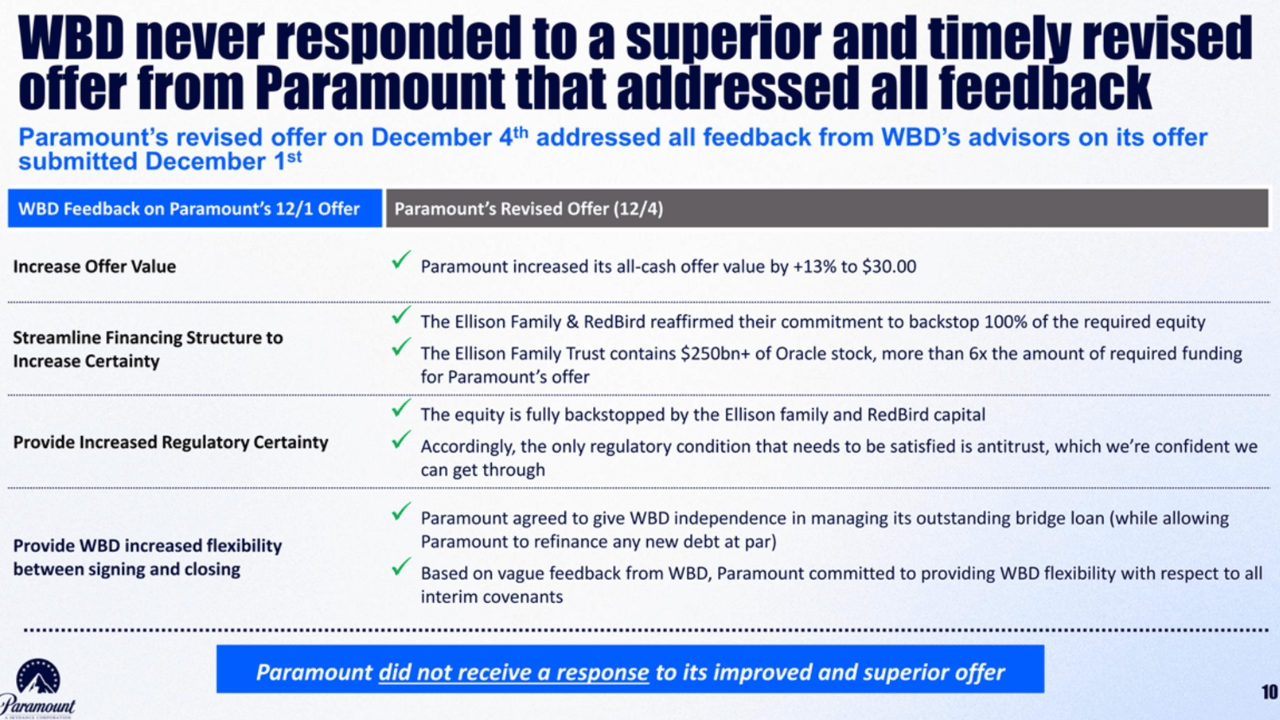

The filing’s timeline, shown on page 10, lays out the events in stark detail. Paramount’s upgraded offer was delivered on December 4th. It resolved the very issues WBD had claimed were obstacles to a deal. It increased value. It clarified financing. It bolstered certainty.

A recap of the offer Paramount made to WBD in an SEC filing – SEC

And yet, WBD provided no response at all.

That lack of engagement becomes even more dubious when paired with what happened next: the Netflix announcement arriving barely a day later. That speed strongly implies the WBD board had already made up its mind—and that Paramount’s improved proposal was never given meaningful consideration.

If that’s true, shareholders were deprived of a legitimate competitive process.

Fiduciary Duties Aren’t Optional

Boards owe shareholders a duty to seek out and evaluate the best available deal. Even if a board prefers one strategic partner over another, it must still weigh competing offers on their merits.

WBD CEO David Zaslav Speaks at a New York Times event – YouTube, New York Times Events

But the Paramount SEC filing paints a picture of a board sprinting toward Netflix while ignoring a materially stronger proposal. Paramount’s revised offer didn’t just raise the headline number. It provided clean, all-cash certainty. It came with fully backstopped financing, including tens of billions already committed. And Paramount argues it carried significantly lower regulatory risk.

When a board rejects such an offer without dialogue, without comparison, and without transparency, the question becomes unavoidable: Was the WBD board acting in the best interest of shareholders—or simply the fastest interest of its preferred partner?

Paramount’s Case: Their Offer Was Clearly Better

Throughout the filing, Paramount lays out why it believes its offer was superior:

- $30 per share, all cash—a higher guaranteed payout

- Faster regulatory approval, according to Paramount’s analysis

- Fully committed financing, including major institutional backing

- Clear operational synergies, shown across multiple slides

Paramount Skydance CEO David Ellison being interviewed – YouTube, CNBC Television

By comparison, the Netflix structure—$23.25 in cash, $4.50 in Netflix stock, and an uncertain spin-off stake—was not guaranteed to equal or exceed Paramount’s value.

And yet, that’s the deal WBD rushed to accept.

Shareholders Deserve to Know Whether They Were Informed

One of the most striking parts of the Paramount SEC presentation is the section encouraging WBD shareholders to ask whether all options were presented to them. Did the board review the improved offer? Did it weigh the financing? Did it assess regulatory risks? Did it examine value differences? Or did it simply block Paramount from participating in the process?

A Paramount SEC Filing on questions WBD Shareholders should ask – SEC

If the board never even considered the offer—or worse, never showed it to shareholders—that isn’t just bad optics. It becomes a fundamental question of fairness.

The Paramount SEC Filing Puts WBD’s Process Under a Harsh Spotlight

This filing doesn’t read like a routine competing-bid presentation. It reads like an accusation—one backed by dates, numbers, and an undeniable timeline. Paramount argues in the SEC report that it offered more money, more certainty, and more stability. And WBD ignored it.

Now shareholders are left wondering why.

What’s your opinion on this Paramount SEC filing? Sound off in the comments and let us know!

{kind=link}